Nansen's research team dives into the collapse of Alameda and FTX using blockchain analytics

Introduction

It started with CoinDesk reporting that “There are more FTX tokens among its $8 billion of liabilities: $292 million of “locked FTT.” (The liabilities are dominated by $7.4 billion of loans.).” Next, Alameda Research’s CEO, Caroline Ellison, offered to buy up Binance’s FTX Tokens (FTT) at $22 per token. What followed was undoubtedly one of crypto’s craziest events – the collapse of FTX and Alameda.

So how did this happen? Did the de-pegging of TerraUSD, Luna’s failure, and the bankruptcy of 3AC all lead to FTX and Alameda’s fall from grace?

Or was it mismanagement of risk and misuse of customers’ funds all along?

Nansen has compiled an in-depth analysis using on-chain data to piece together the fallen dominos of FTX and Alameda. Where possible, we aspire to give an objective account backed by on-chain evidence. Our study does not cover potential off-chain events. This research leverages Nansen’s labeling heuristics to track known wallets of the involved entities and verify their actions on-chain, to make sense of what actually happened during the FTX-Alameda debacle.

Methodology

To put it simply, our on-chain analysis uses information from a blockchain ledger to determine the series of events and fund balances related to the fall of FTX and Alameda. Research Analysts examine the transaction data and crypto wallet activities of the involved entities, two primary data sources useful when trying to piece together what had happened.

Using a proven methodology that we had previously used for other on-chain analyses (TerraUSD de-peg, stETH de-peg), we framed our study using a grounded theory approach where a list of wallet balances and transaction volumes processed through these wallets are at the core of this study. Through a review of grey literature such as social media forum threads, media coverage, and podcasts, we narrowed the scope of our study to focus on transactional data in the following timeframes:

- Until May 2019: Early on-chain Alameda involvement in FTX

- August 2019 - January 2020: FTT as FTX-Alameda’s love child

- May 2022 - July 2022: Studying Alameda’s reaction to the UST collapse and its fallout, as well as a potential loan given by FTX with FTT as collateral

- September 2022 - Now: Recent events and fall of FTX and Alameda

We also paid close attention to a set of wallet addresses which we have identified as either FTX’s or Alameda’s, you can see the list of addresses and labels in the Appendix Section.

The report is formatted in three distinct sections. Part 1 acts as a prologue, providing the context to navigate the relationship between FTX, Alameda, and their interactions with the FTX Token (FTT). Part 2 details the interaction and entanglement between FTX and Alameda through some of the significant events in the recent market cycle. Lastly, Part 3 zooms in on the on-chain data, mainly between 2 November and 9 November. We attempt to triangulate popular (online) narratives with the variable on-chain footprints to make sense of FTX’s and Alameda’s positions and holdings during this period.

Original Sin?

It is no secret that Alameda and FTX were both founded by SBF, and had ongoing partnerships. However, it is rumored that FTX was only really started to raise funds for Alameda and the two colluded from the very beginning.

We leveraged on-chain evidence to draw possible interpretations.

May 2019: Early on-chain Alameda involvement in FTX

It is no secret that Alameda was one of, if not the earliest, liquidity providers on FTX. However, this poses a question of how involved the two entities were.

What was observed:

Alameda’s wallet interacted with FTX before it had even launched in May 2019; apart from other CEX addresses, it was the only clearly identifiable counterparty.

What it could mean: Although relatively low in volume (~$160k), this strongly suggests that either Alameda was heavily involved in FTX’s inception or there was no clear separation between Alameda and FTX then - and perhaps, even both.

July 2019 - Jan 2021: Launch of FTT and early distribution

FTT is a utility token for the FTX platform, it does not entitle users to a part of the platform revenue or represent a share in FTX. It is not backed nor does it give control over governance decisions or FTX’s treasury.

Given the ties between Alameda and FTX, it comes as no surprise that Alameda was in FTT’s seed round, but were they more than just regular investors

The FTT listing

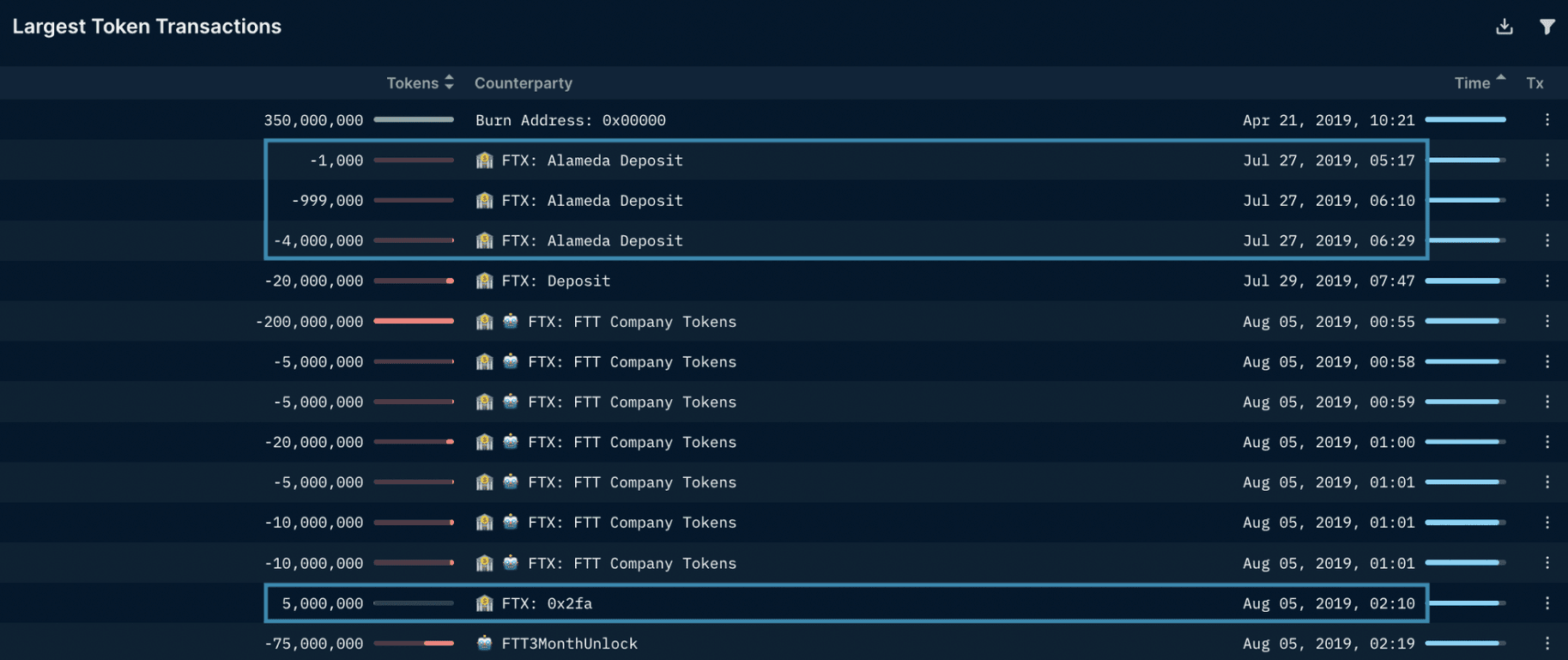

What we observed: Two days before the official listing on FTX on 29 July 2019, Alameda received 5m FTT in three transactions directly from the FTX Deployer (who minted the FTT) to their FTX account. Additionally, 20m FTT were deposited by the FTX Deployer to an FTX-related FTX deposit wallet on the day of the listing. Those were the entirety of FTT in circulation at the time.

Roughly a week after the listing, 5m FTT was sent back to the FTX Deployer on 5 August 2019.

What it could mean:

The 5m FTT returned to the FTX Deployer are likely to be the same ones deposited into the Alameda FTX account.

- The amounts matched perfectly

- Highly unlikely that any other party except FTX itself had this many tokens at the time (20% of the circulating supply)

- As a seed investor, Alameda technically should not have fully transferable tokens at the time in the first place

An optimistic interpretation would be that Alameda was involved in the market-making of FTT tokens. This theory, however, does not explain why the funds were sent back only after a few days.

A pessimistic interpretation would be that Alameda profited off the ICO participants by selling the tokens before other investors’ tokens were unlocked and buying them back cheaper later on to return to FTX.

Following the FTT ICO trail

What we observed:

Using the official token distribution from the FTX docs and comparing it to on-chain movements starting from the first token movements after minting in late July 2019 until December 2020, a likely scenario can be devised for the early distribution of FTT:

Observing the above parameters, we noted some key observations:

- Out of the 350m total supply of FTT, 280m of it was controlled by FTX (~80%).

- Out of the 59.3m tokens for seed and private rounds, presumably in the 3-month vesting contract, around 27m (or roughly 46%) ended up on Alameda’s FTX deposit wallet (see Appendix for details), which is a considerable concentration.

- All of the company tokens (FTT), as well as most unsold non-company tokens, were deposited into a 3-year vesting contract, with an Alameda address as the sole beneficiary.

- 10.7m FTT are unaccounted for, and 10m FTT remain untouched at address 0x4aa.

What it could mean: Our observations raised further questions: Why was there a need for FTX to have such a concentrated supply of tokens? Why would they choose a wallet (Alameda’s) as the beneficiary for the FTT company tokens, that is not directly controlled by FTX themselves?

There was, however, a limitation in the use of on-chain data to surface answers to these questions. Therefore, we focused on what can be answered through on-chain data instead.

Early transaction activity of FTT suggested that:

- Alameda was involved in FTT from day one, and might have even had a significant role in its development

- Almost all the total FTT token supply has to go through Alameda’s hands at some point, due to an Alameda address being the sole and unchangeable beneficiary of the company’s token-vesting contract - this does not mean that Alameda necessarily “owns” the tokens (255m thereof are likely the FTX company tokens) but still is peculiar

- Alameda may have received preferential treatment from FTX

- Alameda and FTX owned the vast majority of the total FTT supply from the very beginning (90%, including the un-moved and unaccounted for tokens), meaning:

- The actual circulating supply (and liquidity depth) is low when compared to the total supply (i.e. low float)

- Prices can be easily influenced to move up (or down) with relatively small amounts when compared to the resulting increase (or decrease) in valuation

- Since both Alameda and FTX held the majority of FTT supply, if one entity is forced to sell its FTT holdings, then the other entity may consequently take a huge hit to its balance sheet

The Good, The Bad, The Bailout

Jan 2021 - December 2021: Shared success in the bull market

Fast forward to the bull market of 2021, the FTT token saw a meteoric rise, roughly 800x from the seed price of $0.10 to $84 at ATH in summer 2021.

The rise in the price of FTT saw the fully diluted valuation of FTT reached almost $30b at the all-time highs - most of which were owned by Alameda and FTX.

Even though the tokens are technically liquid, these quantities would have been impossible to liquidate for Alameda in the open market. Alameda selling could cause wide downward swings in price, and in turn devalue their own remaining positions as well as those of the other holders, with FTX being by far the largest. This was a gordian knot for Alameda’s FTT holdings and created a further co-dependency between Alameda and FTX.

With Alameda not being able to sell its FTT holdings in large quantities, and FTT not generating enough liquid revenue, the potential options for them to obtain liquidity using FTT were:

- OTC: Selling FTT outside the market without impacting the price either by using FTT to make investments (e.g. in venture deals or via an incubator) or sell FTT OTC (e.g. via a market-maker like Genesis).

- LP: Earning by providing liquidity for FTT markets or derivatives (e.g. on FTX).

- Borrow: Using FTT as collateral to borrow against it (e.g. on FTX or Genesis).

Note that many of the ways to access liquidity using FTT were already implemented by FTX from the start, with FTX users as the counterparty.

While OTC selling and liquidity provision are relatively less risky, borrowing against FTT is considered risky as a liquidation event would have a large negative impact on both FTX and Alameda.

So the question remains, did Alameda use the unrealizable book value of their FTT to borrow funds?

What we observed:

There were large FTT transactions between FTX, Alameda, and Genesis Trading:

In September 2021, there were regular inflows and outflows from FTX and Alameda into Genesis Trading. First, we saw an increase in sizable deposits from FTX to Genesis, followed by a significant transfer of FTT tokens from Genesis to Alameda’s FTX address.

It could be possible that FTX sent FTT to Genesis with the intention for the FTT to be used as collateral for a loan to Alameda. However, if this assumption was true then why did Genesis send Alameda the 20m FTT ($1.6b) instead of other, more liquid tokens? As the tokens were not sold, what did they do with them at Genesis, as such a short period of time is not typical for a loan?

Then, in December 2021, Alameda sent a large FTT deposit to Genesis Trading wallet, totaling approximately 38m FTT or $1.7b at the time:

What this could mean:

Alameda could have either tried to sell some FTT OTC to Genesis, or tried to use the transferred FTT as collateral for a loan from Genesis. However, as Genesis is a centralized platform, we are unable to determine this primarily using our on-chain data sources.

Additionally, specific outflows from centralized platforms such as Genesis are hard to trace on-chain, hence, it is challenging to pinpoint exactly how much Alameda had potentially borrowed.

Alameda was also observed to be using FTT as collateral to borrow funds on DeFi platforms such as Abracadabra Money (MIM), though possibly on a much smaller scale compared to their interactions with CeFi lenders such as Genesis.

The on-chain data for FTT so far hints at the following strategy:

However, by utilizing this strategy - taking out loans with FTT as collateral and using the loan to make further investments - would have put them effectively in a leveraged long position.

FTT would have been a central weakness for Alameda and FTX, with price drops posing a very real threat. The rather thin liquidity compared to total supply would have made large market sales very dangerous (e.g. through liquidation of Alameda’s borrowing positions, the bankruptcy of companies that own a lot of FTT, or “dumping” by other large holders like Binance).

May 2022 - June 2022: Potential crisis

Whilst this strategy may have worked well in the bull market of 2021, it may have turned sour when markets started to go against their favor, especially during the May/June 2022 crash:

- OTC: Demand to buy OTC decreases

- LP: Volume, fees and especially buy-side demand for FTT dry up

- Borrow: With FTT prices falling, FTT collateralized loans become riskier. Furthermore borrowing liquidity is drying up, borrowing rates increase (& margin calls), and creditors recall their loans due to general market conditions worsening.

Given that significant portions of Alameda’s balance sheet had consisted of illiquid assets, Alameda may have faced serious liquidity challenges during the May/June 2022 period.

With the UST de-peg and how the situation had unfolded, many entities were adversely impacted then. For full coverage of how the UST de-peg unfolded and the entities involved, our team had covered the situation in-depth here.

The ensuing contagion took down 3AC and Celsius in mid-June 2022 which we had covered in this report; both were debtors to Genesis (who may potentially have had exposure to Alameda based on their on-chain interactions involving the FTT token).

So did Alameda face a liquidity crunch in June, following the 3AC and Celsius collapse? Was there an increase in FTT token activity by Alameda and its counterparts?

What we observed:

Breaking down the chain of events, this is a short run-down of what we had observed on-chain:

Between June 9-23, Alameda received a large inflow of FTT from five various entities: Fund:0xf155, Huobi, Genesis Trading OTC, High Balance, and Found on Avalanche.

June 9 High Balance received 2.7m FTT ($78m) from Celsius: Wallet, which was sent to Alameda FTX deposit.

June 10 High Balance received another 1.6m FTT ($45.6m) from Celsius: Wallet, which was also sent to Alameda’s FTX deposit. The spike of FTT inflow to High Balance wallet was evident on both June 9 and June 10 (as seen in the screenshot below).

June 13 High Balance received another 600k FTT ($14.6m) which was sent to Alameda FTX deposit.

June 14 Fund:0xf155 generally receives their FTT tokens from FTX and BlockFi which is sent out to Alameda’s wallet, including 27.5m ($631m) FTT from FTX which was then immediately sent back to FTX.

Genesis Trading: OTC desk sent 3.7m FTT ($89m) to Alameda FTX deposit.

June 15 Huobi sent a total of 788k FTT ($18.9m) to Alameda FTX deposit.

June 16 Fund: 0xf155 received 14m FTT ($326m) and it was sent directly to Alameda FTX deposit.

June 17 Alameda FTX deposit received 6.2m FTT ($151m) from Genesis Trading: OTC desk and 18m FTT ($450m) from Fund: 0xf155, which they had received earlier that day.

June 18 Fund: 0xf155 sent 27m FTT ($631m) to Alameda FTX deposit.

June 20 Genesis Trading: OTC desk sent a total of 13.6m FTT ($364m) to Alameda FTX deposit.

June 21 Found on Avalanche sent 2.3m FTT ($63m) to Alameda FTX deposit.

June 22 Alameda FTX deposit received 408k FTT ($11m) from High Balance and 249k FTT ($6m) from Found on Avalanche.

June 23 Genesis Trading: OTC desk sent 14.5m FTT ($381m) to Alameda FTX deposit.

June 29

Huobi sends the largest number of FTT to Alameda FTX deposits since the Terra / UST crisis. A total of 18.4m FTT ($47.2m) was transferred.

June 14 - July 1

Between June 14 and July 1, Genesis sent a total of 184.5m FTT ($1.52b) to Alameda’s FTX Deposit. The significant on-chain transfer volumes may suggest that Genesis was potentially a key lender to Alameda.

June 2022: Saving Alameda through an FTT-backed loan?

Indeed, if Alameda had liquidity issues, they could have been in a very tight spot with limited options for orderly liquidating its assets to meet capital requirements.

With lenders generally being cautious after the 3AC crisis, borrowing directly from FTX may have seemed like the only straightforward lifeline to avoid bankruptcy:

- Alameda and FTX have a very close relationship and possibly blurred lines between the organizational structure

- FTX has vested interest in Alameda surviving

- Alameda as a large market-maker on its platform

- Bankruptcy of Alameda would have meant the eventual liquidation of FTT and other token holdings, spelling the de-facto death of FTX’s FTT holdings (~$20b at peak)

- FTX had access to large reserves of liquid assets (i.e. user funds)

According to the latest report by New York Times on How Sam Bankman-Fried’s Crypto Empire collapsed, Alameda’s CEO confirmed that “over the recent months, Alameda had taken out loans and used the money to make VC investments, among other expenditures.” Alameda CEO also confirmed that “around the time the crypto markets crashed this spring, lenders moved to recall those loans but the funds that Alameda spent was no longer easily available.” As a result, Alameda resorted to FTX’s customer funds to make the payments.

Did Alameda really receive an FTT-backed loan from FTX?

We looked at FTT deposits from Alameda onto FTX which could have been posted as collateral, as well as non-FTT outflows from FTX to Alameda.

Posting FTT as collateral

What we saw:

There were massive net FTT inflows from Alameda to FTX during mid-June, coinciding with the 3AC collapse, totaling 163m FTT, worth around $4b at the time.

It is difficult to correctly attribute outflows from centralized platforms into entities on-chain, and some of these funds might have circled back to Alameda directly or via a third party and back to FTX again. Therefore, the net values displayed in the chart may likely be higher than the actual net inflow.

A look at FTX’s user fund wallet reveals, however, that the balance on FTX rose from 14m FTT to 54m FTT, an increase of 40m FTT, ~$1.2b from mid-June to mid-July, most of which can be attributed to Alameda.

What this could mean:

Alameda deposited as much as ~$4b (based on mapped net inflows) worth of FTT tokens on FTX between early June and July, with the peak being during the 3AC collapse in the week of 12 June 2022.

This is in line with the interview from Reuters with several people close to Bankman-Fried, revealing a $4b loan from FTX to Alameda backed by FTT tokens, Robinhood shares, and other assets.

Loans from FTX

The question of whether FTX provided funds to Alameda, cannot be conclusively answered by on-chain data alone.

FTX could have sent the funds to any recipient, including the creditor directly, in any token, on (almost) any chain as well as provided the funds completely off-chain.

Furthermore, looking at wallet balance changes is inconclusive as well.

As for the FTX wallet balances, many withdrew funds from the exchange during these turbulent times, leading to high fluctuations in the total balance. Additionally, it is unclear what the actual balance of funds should have been, so determining a potential delta is also not an option.

What could be seen were various token flows between FTX and Alameda with values ranging from tens of thousands to tens of millions in USD value. While we did observe a few unusually large transactions with transaction values in the hundreds of millions in USD value, we did not have sufficient evidence to triangulate and deem these transactions to be “suspicious” or to fully back the theory.

However, it remains a mystery as to what was the purpose of these following large transactions.

- On 12 May 2022, FTX transferred 90k ETH ($211m) + 6.8m FTT ($224.7m) to Alameda: 0x780 and transferred them to Genesis. The 6.8m FTT was received from the High Balance wallet, funded by Celsius.

- On 12 May 2022, FTX sent another 155,443 ETH ($323.4m) to Alameda 0x780 which was eventually transferred to Genesis once more.

- On 26 May 2022, FTX sent 3.5m FTT ($103m) to Alameda Research: 0x780, which was eventually transferred to Genesis once more.

To Fall, Falter, and Fail: SBF’s Crypto Empire Collapses

We summarized the events that caused the “death-spiral” of both FTX and Alameda:

Sept 28 All withdrawals from the FTT company tokens vesting contract have to go through this Alameda wallet as it is declared the only beneficiary from the start (see Appendix). Still, them withdrawing all of the remaining tokens and sending them to FTX Deployer leaves a sour taste in light of the loan agreement.

Oct 31- Nov 1 An unusual list of continuous stablecoin transfers from FTX International and FTX US to Alameda’s Circle, Binance and FTX wallet was spotted. These stablecoins included USDC, BUSD, TUSD,PAX,TUSD and amounted to a total of $388m USD.

Nov 2 Coindesk releases a report on Alameda’s balance sheet. It revealed that $5.8b of the $14.6b assets on Alameda’s balance sheet were reportedly in FTT and other Solana ecosystem tokens. The majority of net equity in Alameda’s business was actually FTX’s own centrally-controlled token, FTT.

Nov 6

Alameda CEO makes a statement on the balance sheet report from Coindesk and clarifies that Alameda had >$10b of assets that were not reflected in the piece. She does not shed light on liabilities that were not listed in the report. The Tweet has since been deleted, and we were not able to fully verify her claim on-chain.

Binance CEO announces that they have decided to liquidate the remaining FTT on their books, worth ~$584m in FTT.

Alameda CEO offers to OTC buy all of Binance’s FTT holdings for $22 per token, leading to speculation that Alameda may have had loans that would have otherwise been liquidated if the price of FTT falls below $22. This Tweet has since been deleted.

The review of identified Alameda wallets on the Ethereum chain suggested that Alameda’s holdings on the Ethereum chain were approximately valued at $21m on 6 Nov 2022 (based on available Nansen data) . Scrutiny of the on-chain data revealed that it was highly unlikely that Alameda had the liquidity to purchase Binance’s FTT when Caroline tweeted publicly on 2 Nov 2022. So then, what was the motivation behind Caroline's public offer to purchase Binance’s FTTs?

Wallet balances obtained are based on available Nansen data. Actual wallet balances may be higher (e.g. does not take into account LP tokens and/or Alameda’s balances on CEXs)

Binance CEO reinforces a statement on liquidating their FTT holdings. There was no on-chain activity to support this move at the time at which the statement was made.

FTX CEO responded by clarifying that FTX is solvent, stating that “FTX is fine, assets are fine.” This Tweet has now been deleted.

Nov 7 Markets resort to panic mode. Nansen’s tracking of the 7-day stablecoin flows showed a net inflow of $411.5m deposited into Binance, with a net outflow of $451.1m in withdrawals from FTX in that period.

Additionally, our on-chain examination brought to attention a list of (unusually) large withdrawals prior to FTX’s collapse.

Entities who withdrew significant amounts 24 hours before withdrawals were halted:

| Receiving wallet | Net withdrawals | Receiving address |

|---|---|---|

| ETH Millionaire | $245,073,409.42 | 0xbe385b59931c7fc144420f6c707027d4c2d37a81 |

| FTX Exploiter: 0x59ab | $26,263,554.91 | 0x59abf3837fa962d6853b4cc0a19513aa031fd32b |

| Token Millionaire | $13,367,016.79 | 0xd952beecffc6bc1228e83d0457d25d5a39555abf |

| Token Millionaire | $11,996,046.63 | 0xd04aa3a5a0518ba1dea0d48ff21c57e8f20ba753 |

| ETH Millionaire | $9,995,037.45 | 0x33566c9d8be6cf0b23795e0d380e112be9d75836 |

| Token Millionaire | $9,995,036.95 | 0x98f67ae22745fdfe2e03637b248ea30c4d0a2394 |

| "BobbieDigital" on OpenSea | $9,737,856.51 | 0x2c071af9dcefb7155659b662480cbb8679977394 |

| FTX withdrawer after freeze | $9,045,039.76 | 0x26c5a34bc8398fbd395b518ffab27724d7cc9617 |

| 🏦 Binance: Deposit | $8,925,449.94 | 0x8dfc08a8ca0c4a20c19a60e3d1793aafdfe3fda1 |

| 🏦 Binance: Deposit | $8,911,052.29 | 0x78b20f9b17a6ea64f031f7783fc01bb6c73d9324 |

| 🏦 Coinbase: Deposit | $8,830,227.22 | 0x982603136ea0efba1343c050730338321c6dfe44 |

The immense sell-pressure of FTT meant that the token eventually broke lower than $22 per token.

Nov 8 FTX appeared to have paused withdrawals as reported by The Block. During this period, FTX sent 92m ($37m) of BIT to 🤓 Alameda Research: 0x84d.

FTX CEO shared that Binance would enter into a strategic transaction with FTX, of which Binance CEO announced a non-binding Letter of Intent to fully acquire FTX and help cover its liquidity crunch.

It appeared that Binance was leaning towards scrapping FTX rescue takeover after taking first glance at books. At this point in the timeline, FTX US had sent $10m USDT to Alameda. Alameda Research then sent 130k FTT (~$715k) to 🏦 Binance: Alameda Deposit. Lastly, FTX US sent 2,262 WBTC ($41m) to 🤓 Alameda Research: WBTC which was later sent to WBTC: Controller. It is interesting to note that while FTX International had halted withdrawals, FTX US still managed to transfer a sizable amount of WBTC to Alameda. Alameda CEO also implied that only the FTX International entity was facing liquidity issues and that FTX US was unaffected.

Nov 9 The Wall Street Journal reported that Binance had walked away from the FTX deal.

Nov 11 FTX filed for Chapter 11 bankruptcy proceedings, with the FTX CEO resigning

According to an unverified insider source that was leaked on Twitter as of 16 Nov, “Caroline painted Alameda and FTX getting liquidated as a likely event rather than a tail event.” Moreover, FTX’s native token FTT was also a focal point contributing to the fallout. The low float and constant buy pressure from FTX implied that the only thing that could potentially trigger the FTT price to go down was a massive sell pressure for the token. While the Coindesk report first garnered the public’s attention to the relationship between Alameda & FTX, the “bank-run” on FTX had also coincided with the announcement that Binance was looking to liquidate the remaining FTT on their books.

Piecing together the pieces from our on-chain investigation, it was evident that the Luna/Terra collapse revealed a deep flaw between Alameda and FTX’s muddled relationship. There were significant FTT outflows from Alameda to FTX around the Terra-Luna/ 3AC situation. Based on the data, the total $4b FTT outflows from Alameda to FTX in June and July could possibly have been the provision of collateral that was used to secure the loans (worth at least $4b) in May / June that was revealed by several people close to Bankman-Fried in a Reuters interview.

We also observed slightly unusual large continuous outflows of stablecoin tokens from FTX to Alameda’s wallets during that time period. Given the cascading effect of the Luna collapse, many firms like 3AC were liquidated causing a contagion across the crypto lending market. While our on-chain investigation did not directly verify that user funds were being siphoned from FTX to Alameda in attempts to “save” them from liquidation, the unusually large FTT inflows from FTX post-Luna/ 3AC hint at a plausible case.

From this point on, the intermingled relationship between Alameda and FTX became more troubling, given that customer funds were also in the equation. Alameda was at the stage where survival was its chosen priority, and if one entity collapses, more trouble could start brewing for FTX. Given how intertwined these entities were set up to operate, along with the over-leverage of collateral, our post-mortem on-chain analysis hints that the eventual collapse of Alameda (and the resulting impact on FTX) was, perhaps, inevitable.

The sudden fallout of FTX had induced a growing fear within the crypto market participants - both investors and traders alike. If anything, this situation only strengthens the need for more transparency in crypto. Our team at Nansen Portfolio have compiled real-time dashboards that showcase crypto exchanges’ proof-of-reserves. Whilst the list of asset holdings is non-exhaustive, this is the first step to holding crypto participants more accountable. Link to proof-of-reserves per entity by Nansen can be found here.

The Epilogue: Interesting Entities and Wallets

During our investigation we noted a set of wallets that may or may not be Alameda/ FTX’s addresses. Observation of on-chain activities and interactions hint at a high likelihood that these wallets had an indirect exposure with Alameda. For those who are interested in exploring these wallets, we have provided a brief description of the relevant activities.

To get a better understanding of our wallet labels, read more here.

| Address | Description |

|---|---|

| High Balance | • Throughout our analysis, we found out that High Balance gets all their FTT tokens primarily from Celsius Trading: Wallet. Significant transfers were all sent out to FTX: Alameda Deposit. High Balance is perhaps an intermediary address that helps with facilitating transfers between Celsius Trading: Wallet and FTX: Alameda Deposit. • On May 11 2022, High Balance received 6.8m FTT ($255m) from Celsius: Wallet which was sent out to Alameda FTX deposit. • On May 12 2022, High Balance received 881k FTT ($25m) from Celsius: Wallet which was sent out to Alameda FTX deposit. • High Balance sent a total of 6.8m FTT ($190.3m) to FTX Alameda Deposit from May 27 onwards up until July 13 (during LUNA/ UST contagion). |

| Fund: 0xf155 | • Fund: 0xf155 sent a total of 88m FTT to FTX: Alameda deposit from the period of 14 June to 13 July, 2022. The relationship between Fund: 0xf155 is opaque. • Based on on-chain evidence, this address received $403m worth of FTT tokens and sent out the same amount in cumulative value. This wallet is potentially used for intermediary transactions, seeing as most of the transactions with Alameda wallets are transactions out. • Tracing their previous transactions, FTX often sends FTT tokens to Fund: 0xf155 which is then sent to Alameda Research: 0x84d and is transferred to another Alameda Wallet, perhaps to obfuscate their traces or for other unknown purposes. The FTT ends up back in FTX. Besides receiving their FTT from FTX, Fund: 0xf155 also received 2.54m FTT from Medium Dex Trader (that originated from BlockFi). • High Balance sent a total of 6.8m FTT ($190.3m) to FTX Alameda Deposit from May 27 onwards up until July 13 (during LUNA/ UST contagion). |

| Found on BSC | • “Found on BSC” address only interacted once with Alameda on 27 June 2022, who sent 3.2m FTT ($87m) to FTX: Alameda Deposit. • This address interacted with several FTX-related wallets. All of the token transactions to “Found on BSC” are funded from FTX. Diving deeper into the interactions between FTX and “Found on BSC” and which tokens are sent into “Found on BSC” wallet, FTT and SRM stand out. |

| ETH Millionaire | • ETH Millionaire transferred a total of 1m FTT ($24.4m) to FTX Alameda wallet from June 14 - Nov 7, 2022 • FTT tokens transferred by ETH Millionaire came from Bitgo Forwarder which also received their FTT tokens from Genesis Trading OTC Desk. |

| Huobi | • Huobi sent 788k FTT to FTX Alameda wallet on June 15 alone. • While such FTT flows between Huobi and FTX:Alameda is not unusual, the amount of FTT transferred on June 15 was above the daily average of 278.4k FTT tokens transferred since May 2022. • On 29 June 2022, Huobi sends the largest number of FTT to FTX: Alameda since the Luna and UST Crash • Total of 1.84m FTT Tokens ($47.2m) were transferred. • Huobi also receives huge amounts of FTT tokens from FTX, possibly for market-making activities. From May 1 to Aug 17, FTX sent a total of 4.98m FTT tokens worth $139m to Huobi. |

| Genesis Trading: OTC | • Between June 14 and Aug 16, Genesis Trading: OTC sent a total of 95.4m FTT ($2.5b) to FTX Alameda. • Such volume could possibly indicate a strong relationship between Genesis and Alameda. |

Appendix

Mapping process of official FTT distribution to on-chain movements and addresses

350m minted in total and distributed in late July 2019 by Deployer and from there:

5m goes straight to Alameda’s FTX Deposit before FTT token listing on FTX and 5m was returned from FTX shorty after the listing

5m tokens was transferred to FTX: 0x2fa and likely gets credited to Alameda’s FTX account

Source: Nansen 5m returned from FTX: 0x2fa 6 days after launch. Probably the same tokens from Alameda as no one else should have this size at this point and there would be no reason for FTX to withdraw tokens. These transactions sum up to net 0 and the tokens end up back at the FTX deployer and then in the 3month vesting contract.

20m gets transferred to FTX Deposit: 0x23b

- Likely the funds for Liquidity provision as stated in the tokenomics

255m FTT tokens allocated to FTT Company Unlock Smart Contract

- 175m FTT to FTX (almost certain) + 105m FTT transferred to other entities and not sold (almost certain) - 20m FTT as initial liquidity (almost certain) - 5m FTT to Advisors = 255m

- Unlocks linearly but has to be claimed and if left untouched, the “claimable amount” just increases until it is claimed (see contract details)

- The sole beneficiary of the contract is this Alameda wallet (see contract details and withdrawals from the FTT Company Token Contract) which sends it all back to the FTX deployer (who sends it to FTX) except for 9m to Millionaire: 0xef9

- 72m have been withdrawn until mid April 2020 and sent to Alameda wallet and then to FTX deployer who puts most of it on FTX

- Unknown what happens after that

- 173m have been withdrawn at once September 28, 2022, and then sent to FTX deployer and then with some other remaining FTT to FTX Withdrawer After Freeze after the FTX collapse

Judging by the number, these are almost certainly the FTX company and FTX company administrated tokens. The Alameda address being the only beneficiary of the vesting contract is a sign of a very close connection between the companies. If the Alameda wallet receives FTT from the contract they likely actually belong to FTX. They usually forward them at some point and do nothing with them.

- 75m into 3month unlock contract

- 59.3m to Investor rounds (almost certain) + 5m to Advisors (likely) + 10.7m unaccounted from tokenomics document (likely)

- From 3month unlock contract everything went to Heavy DEX trader: 0x55b and from there:

5m back to FTX Deployer which ended up on FTX deposits 0xa5d and 0x23b, could be Advisor tokens or a mix of advisor and early investors (likely)

10m to Token Millionaire: 0x4aa (sits there till today)

20m to FTX Deposit:0xa5d (same one the FTX Deployer deposited in, likely affiliated with FTX and/or Alameda), tokens likely distributed to FTT early investors, distributed via the FTX platform

40m to token Millionaire: 0xef9, who also received 9m from Alameda around the same time

- 1.5m FTT still remains there

- 20m to FTX Deposit: 0xa5d (same where the 3mo unlock went and FTX deployer sent funds as well), Further distribution to early FTT investors (likely)

27.5m to EIP1559 user: 0x209 who sends:

- 13.5m to EIP1559: 0xf27 who sends 13m to FTX: Alameda Deposit and 500k to High Balance: 0x648 where it still remains

- 14m to FTX: Alameda Deposit

- Alameda as a seed investor likely received at least 27m FTT on initial distribution, being around 8% of the total supply and 46% of the tokens sold during the raise.

Overall it is likely that at least 307m tokens out of 355m tokens (86%) of all FTT were initially controlled by Alameda or FTX. With another 12m tokens not being distributed and remaining untouched throughout the years in wallets with unknown owners, this percentage could be as high as ~90%.

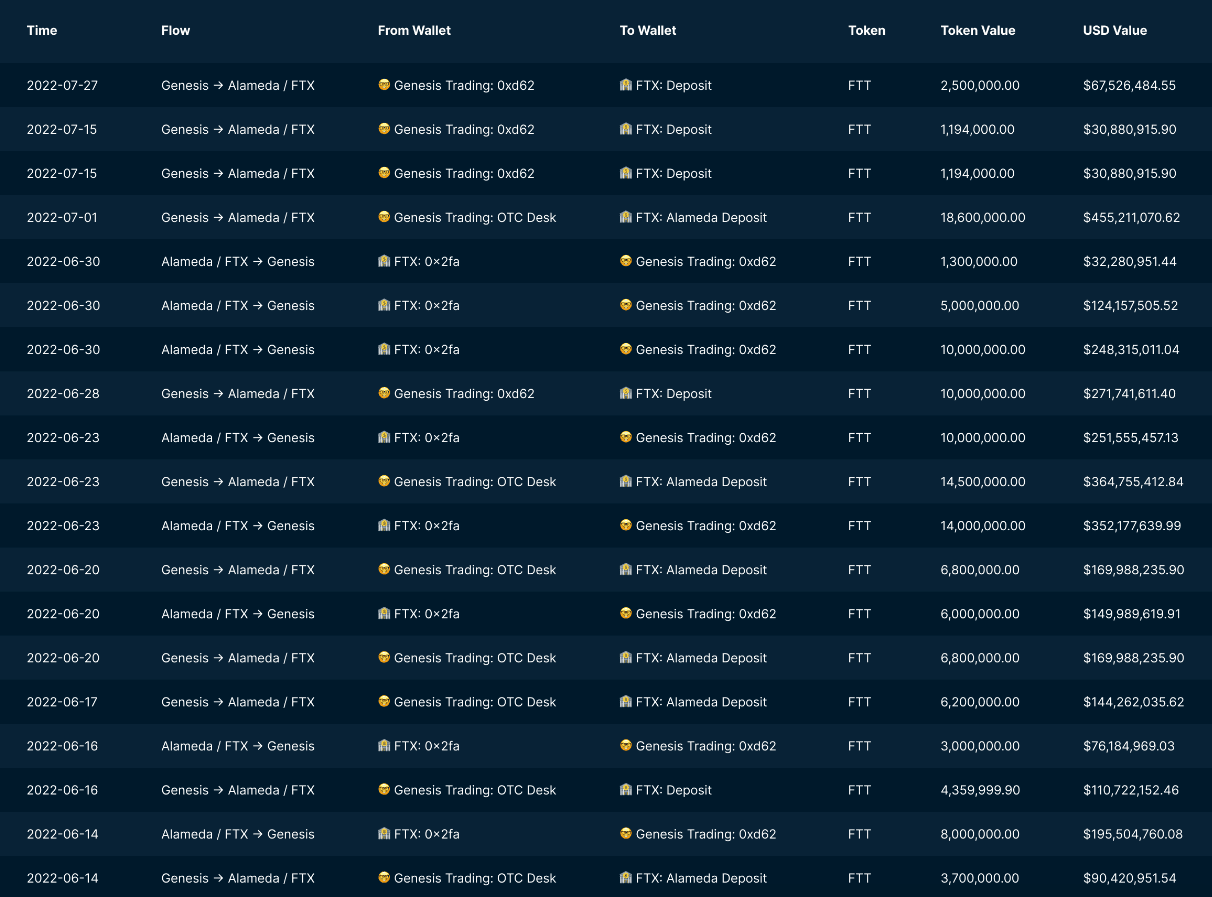

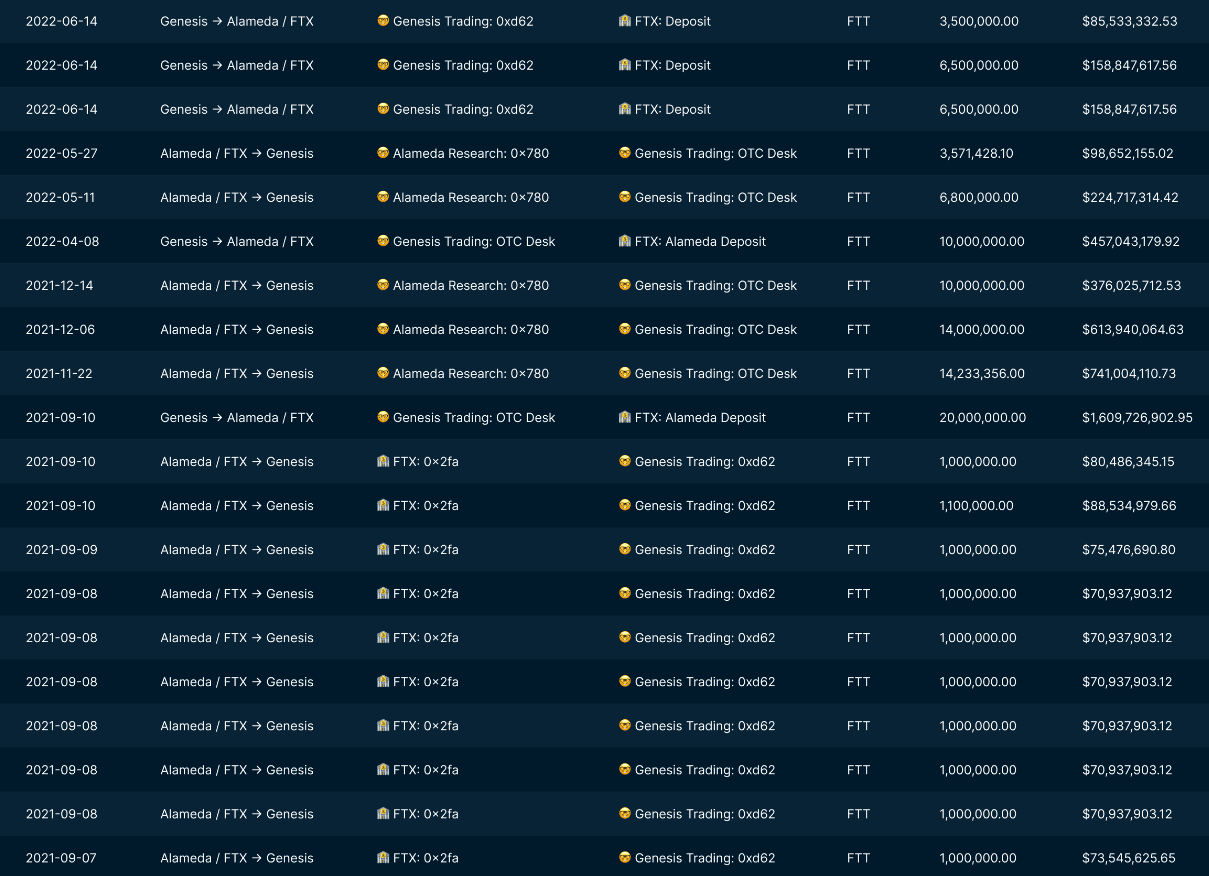

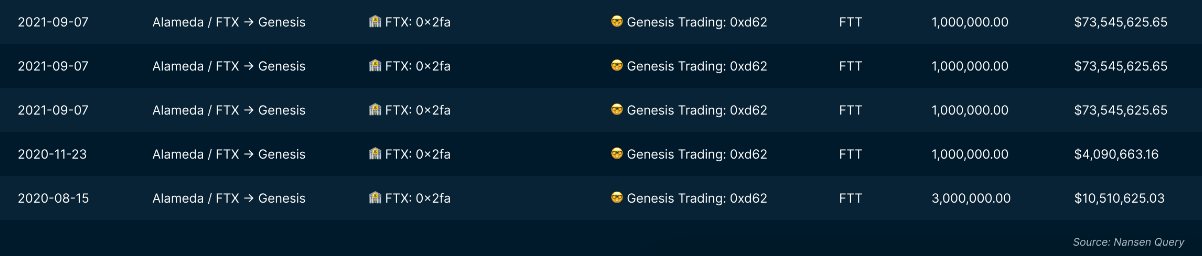

Alameda / FTX FTT transactions with Genesis Trading

Nansen wallet labels and addresses